A meta’ dicembre abbiamo letto gli sviluppi della fusione Cantine Riunite – CIV (+Coltiva), che ha portato all’acquisizione delle quote di minoranza di GIV e al completamento dell’acquisizione di Bolla. Nasce cosi’ il leader italiano nel mondo del vino, con un fatturato 2008 pro-forma che stimiamo a EUR470-480m. Oggi vi propongo una piccola analisi del nuovo gruppo che ha dalla sua parte una buona dimensione (per quanto ancora molto lontana dai leader mondiali, tra i quali l’Italia del vino meriterebbe di stare) e una ottima segmentazione di prodotto. Dall’altra parte, il nuovo gruppo mantiene lo status di cooperativa, il che significa che i soldi li fanno sempre i soci e mai l’azienda, che quindi non e’ in grado di adottare una corretta politica di autofinanziamento. Infine abbiamo dato un’occhiata alla valutazione della vendita di quote del GIV. Se le indiscrezioni di stampa sono corrette, l’operazione e’ stata compiuta a un multiplo del fatturato (2007 e 2008) di circa 1.2x e a un multiplo del MOL (2007) di circa 16x. Quest’ultimo multiplo sembra elevato, ma dobbiamo considerare che il margine di GIV (7%) e’ ben al di sotto di quello che dovrebbe essere se fosse gestita come un’azienda, il che significa che si tratta di una valutazione che si puo’ adottare soltanto per le entita’ cooperative.

In mid December we read about the developments of the merger Cantine Riunite – CIV (+ Coltiva), which led to the acquisition of minority interests of GIV and the completion of the acquisition of Bolla. As a result, the Italian leader in wine business was formed, with a pro-forma 2008 turnover of EUR470-480m. Today I propose an analysis of the new group that has on his side a good size (although still very far from world leaders) and an excellent product segmentation. On the other hand, the new group maintains the status of cooperative, which means that the cash generation is always withdrawn by the shareholders and the company cannot reinvest its profits. Finally, we looked at the valuation of the disposal of GIV minority stakes. If the rumours about the price are correct, the operation was performed at a multiple of revenues (2007 and 2008) of approximately 1.2x and a multiple of EBITDA (2007) of approximately 16x. The latter seems high, but we must consider that the margin of GIV (7%) is well below what it should be as if it would be a normal firm, which means that this multiple is reliable only for valuation in the world of cooperatives.

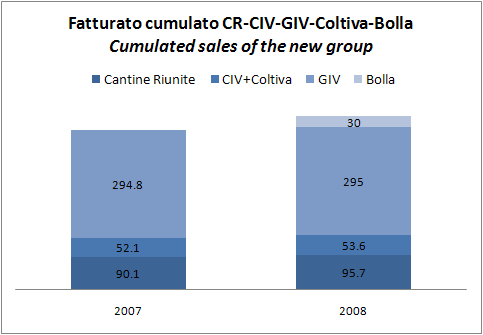

Partiamo con i numeri. Il fatturato “pro-forma” 2008 (cioe’ un numero artificiale che dovrebbe pero’ dare l’idea di come potrebbe essere il prossimo anno) del nuovo gruppo dovrebbe essere di circa EUR474m, considerando anche Bolla. All’interno del nuovo gruppo, il 62% delle vendite fa capo al GIV, circa il 20% a Cantine Riunite, l’11% a CIV-Coltiva e il rimanente 6% sara’ apportato da Bolla (utilizzando le vendite dichiarate da Brown Foreman tradotte in euro). I volumi di vendita dovrebbero essere imponenti: stiamo parlando di 18m di casse da 9 litri a un prezzo medio di EUR2 per bottiglia (EUR24 per cassa). Nel secondo grafico potete vedere come si posizionano le diverse aziende: GIV copre l’alto di gamma con un prezzo di EUR3.4 per bottiglia, Bolla e’ a EUR1.9, mentre CIV e Cantine Riunite sono a EUR1.3.

The pro-forma turnover 2008 (ie an artificial number that should set an idea of how it could be next year) of the new group should be EUR474m, considering also Bolla. Within the new group, 62% of sales are generate by GIV, about 20% from Cantine Riunite, 11% for CIV-Coltiva and the remaining 6% will be provided by Bolla (using sales reported by Brown Foreman translated into euros). The sales volumes should be impressive: we are talking about 18m 9 liters cases at an average price of EUR2 per bottle (EUR24 per case). In the second graph you can see how the 4 contributors are segmented by price: EUR3.4 per bottle for GIV, EUR1.9 for Bolla, while CIV and Cantine Riunite are at EUR1.3.

Un secondo punto di vista e’ rappresentato dalla dimensione rispetto ai concorrenti italiani. E qui vi presento una classifica di fatturato 2007 con il nuovo gruppo in rosso e i 3 gruppi che gia’ figuravano nella classifica Mediobanca dei primi gruppi vinicoli italiani in bianco. Il divario con il secondo (Caviro, includendo la produzione di alcol) e’ piuttosto significativo. Non sara’ cosi’ nelle classifiche per utili: nel 2007 GIV ha prodotto EUR11m di utile operativo, Cantine Riunite circa EUR7m. Non conosciamo i numeri di Bolla e di CIV, ma e’ difficile che queste due possano consentire al gruppo di superare EUR25-30m: resteranno sicuramente molto indietro rispetto al leader italiano Antinori (EUR40m) e probabilmente supereranno il numero 2 Santa Margherita). Proprio qui sta il principale rammarico: un’azienda di queste dimensioni, se non fosse una cooperativa genererebbe un autofinanziamento (a occhio almeno 50-60 milioni) tale da potersi comperare ogni anno una media-grande cantina italiana… ma con lo status di cooperativa i soci si portano via tutto…

A second point of view is represented the size compared to Italians competitors. And here we present a ranking of 2007 turnover with the new group in red and the 3 forming groups already included in the ranking in white. The gap with the second (Caviro, including the production of alcohol) is quite significant. The ranking for profits will look very different: GIV reported in 2007 an operating profit of EUR11m, Cantine Riunite about EUR7m. We do not know the numbers of Bolla and CIV, but it is unlikely that these two can allow the group to exceed EUR25-30m: surely the new group will remain well behind the leader Antinori (EUR40m) but probably it will exceed the number 2 Santa Margherita. This is the main disappointment: a company of this size, if not a cooperative would generate a self financing (at least 50-60 million) which would be enough to buy each year an average-sized Italian winery… but with the status of cooperative suppliers-shareholders will take away everything …

Mi scuso per il post lungo, ma facciamo anche il punto sulla valutazione dell’operazione di riacquisto delle minoranze di GIV. Si parla di EUR80m per il 35%, il che implicherebbe un valore d’impresa (compreso il debito 2007) di circa EUR340-350m. Cioe’ circa 1.2 volte il fatturato e 16 volte il MOL. Da una parte va considerato che si tratta di un’operazione sulle minoranze (che vale quindi meno di un’operazione sulla maggioranza), dall’altra che si tratta di una cooperativa: se posso permettermi, il multiplo piu’ interessante ed esportabile e’ quello sul fatturato.

I apologize for the long post, but I also make a point on the evaluation of the repurchase of minorities of GIV. The rumour is EUR80m for 35%, which means an enterprise value (including debt 2007) of around EUR340-350m. It means about 1.2 times sales and 16 times EBITDA. On one side it should be noted that this is a minority stake (then worth less than a majority stake), on the other side that it is a cooperative.

[TABLE=108]