Oggi vi riporto in Nuova Zelanda per iniziare a coprire una azienda, Delegat’s, che e’ il piu’ importante esportatore di vino della Nuova Zelanda. Non solo, e’ anche una azienda che sta investendo pesantemente (cioe’ oltre il 20% del fatturato all’anno!) per ampliare il suo raggio d’azione. E’ una specie di Concha y Toro in miniatura, una specie di ambasciatore del vino NZ nel mondo. Quotato alla borsa di Auckland, vale circa 150m di dollari americani (215m di dollari Neozelandesi). Prima di continuare chiarisco che tutti i numeri che trovate qui dentro sono milioni di dollari della Nuova Zelanda, che valgono circa la meta’ di un euro (cioe’ 100m di dollari NZ sono 50m di euro). Nel 2008 (12 mesi a giugno) ha concluso un altro anno strepitoso, caratterizzato da una crescita del fatturato del 23%, del MOL e dell’utile netto di quasi il 30%. Ma a ben vedere, questa e’ la punta dell’iceberg: Delegat’s praticamente non esisteva prima del 2003: il suo fatturato e’ passato da NZ$22m a NZ$162m nell’arco di soli 5 anni.

Today we go back to New Zealand to begin to cover a company, Delegat’s, that is the most important exporter of wine from New Zealand. Not only that, it is a company that is investing heavily (like over 20% of sales a year!) to grow its size. It is a kind of Concha y Toro in miniature, a sort of ambassador of NZ wine in the world. Listed on the Stock Exchange of Auckland, it is worth about 150m US dollars (215m New Zealand dollars). Before continuing I clarify that all the numbers you find here are millions of dollars of New Zealand, which are half of the value of the euro (ie 100m NZ dollars are 50m euros). 2008 (12 months to June) was a great year, characterized by a growth in turnover of 23% and of EBITDA and net income by almost 30%. This is just the peak of the iceberg: Delegat’s practically did not exist before 2003: its turnover rose from 22m NZ $ to NZ$162m in just 5 years.

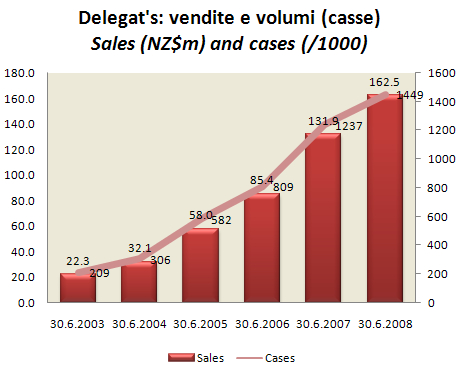

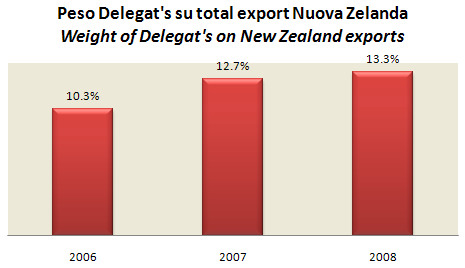

Come dicevamo, l’azienda e’ un forte punto di riferimento per le esportazioni: Delegat’s ha raggiunto il 13% di tutto l’export della Nuova Zelanda, grazie a un prezzo medio di vendita ben superiore alla media (oltre 100NZ$ per cassa contro 80-90 del mercato). E’ il leader indiscusso del Merlot locale (33% dell’export) ma anche dello Chardonnay (31%), mentre rappresenta il 12.5% delle esportazioni di Sauvignon e il 6% di quelle di Pinot Noir. Come vedete dal primo grafico, vende 1.44m di casse da 9 litri a circa NZ$112 ciascuna, per un fatturato di circa NZ$162m, che sono poi largo circa EUR80m. Dal 2005 in avanti, alla forte progressione dei volumi (grazie agli investimenti) si e’ accoppiato un graduale miglioramento del mix.

As we said, the company is a strong point of reference for exports: Delegat’s reached 13% of all exports from New Zealand, thanks to an average sales price well above the average (over $100 vs 80-90 for the market). It is the undisputed leader of the local Merlot (33% share of exports) but also of Chardonnay (31%), while representing 12.5% of exports of Sauvignon and 6% of Pinot Noir. As you can see from the chart, Delegat’s sold 1.44m 9 liters cases at NZ$112 each, for a turnover of around NZ $162m, which are equal to about EUR80m. From 2005 onwards, the strong progression of volumes (through investment) was coupled a gradual improvement in the mix.

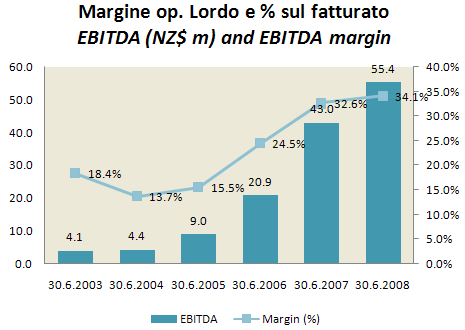

I margini sono quelli del viticoltore: il MOL e’ arrivato a NZ$55m, con una % del 34% sulle vendite. La curva spiega molto meglio l’incremento di margini in relazione alla dimensione. Soltanto 3 anni fa l’azienda guadagnava il 15% del fatturato. Le spese di marketing sono impressionanti: il 24% del fatturato, un livello degno delle piu’ aggressive aziende di superalcolici e ben superiore a qualsiasi azienda italiana che abbia dato tale dettaglio (forse solo Caviro e’ vicina al 20% se prendete solo la divisione vino). L’utile netto cresce in proporzione, frenato dall’aumento degli oneri finanziari: nel 2008 gli azionisti hanno guadagnato NZ$19m da NZ15m del 2007, ma soprattutto rispetto agli NZ$1-2m che l’azienda guadagnava fino al 2005.

The margins are those of a wine farm: the EBITDA is NZ$55m, with a margin of 34%% of sales. The curve explains the increase in margins in relation to its size. Only 3 years ago the company earned just 15% of sales. The marketing costs are impressive: 24% of turnover, a level never seen in any other firm so far (and only Caviro is close to 20% for the wine division). Net income grows in proportion, slowed by financial charges: in 2008 the net profit reached NZ$19m from NZ15m of 2007, compared with NZ $ 1-2m that the company posted until 2005.

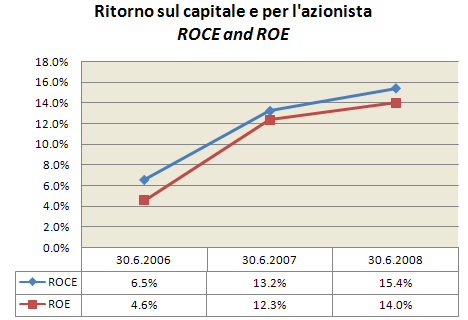

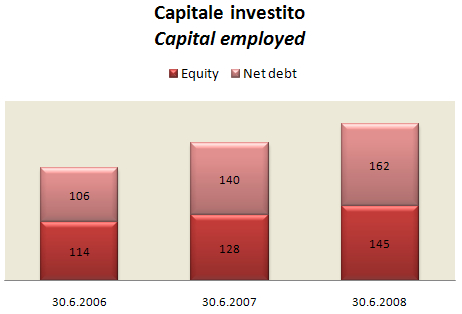

Tutto questo non e’ venuto per caso. Gli investimenti sono stati ingentissimi: NZ$105m nel corso degli ultimi 3 anni soltanto per vigneti e cantine, oltre NZ$40m nel capitale circolante. Cosi’ Delegat’s ha cumulato un debito di NZ$162m, che si confronta con NZ$55m di EBITDA, cioe’ circa 3 volte, in forte miglioramento rispetto al rapporto di 5x di un paio di anni fa. Il ritorno sull’investimento pero’ comincia a vedersi: il ritorno sul capitale prima delle tasse e’ salito al 15%, quello degli azionisti al 14%.

All this was not coming by chance. The investments were enormous: NZ$105m over the past 3 years only for vineyards and wineries, more than NZ$40m in working capital. So, Delegat’s has a cumulative debt of NZ$162m, which compares with NZ$55m of EBITDA, about 3 times, a strong improvement in the ratio of 5x of a couple of years ago. The return on investment is gradually moving up with the return on equity before tax at 15% and ROE of 14%.

Ma quanto vale in borsa Delegat’s? Il capitale azionario vale NZ$215m contro un’attesa di utile netto per giugno 2009 di circa NZ$25m: ne deriva un rapporto prezzo/utile di circa 8.6x. Aggiungendo il debito di circa 160m e gli interessi di minoranza per NZ$60m arriviamo a un valore d’impresa di circa NZ$453m. Con un MOL atteso a NZ$65m per il 2009, il multiplo e’ di circa 6.7x.

But what are Delegat’s market multiples? The share capital is NZ$215m against an expected net profit for June 2009 of around NZ$25m: this means a P/E of approximately 8.6x. By adding debt of about 160m and minority interests of NZ$60m we get to an enterprise value of around NZ$453m. With an expected EBITDA of NZ$65m for 2009, the EV/EBITDA multiple is 6.7x.