I risultati del primo trimestre (marzo-maggio 2007) del colosso mondiale del vino non sono stati particolarmente positivi, anche se stiamo parlando del periodo meno significativo dell’anno. CBrands ha appena deconsolidato l’attivita’ all’ingrosso e relativa alla birra e quindi a partire dal 2007-08 i suoi risultati opertivi sono molto vicini a quelli della divisione vino.

A onore di cronaca va detto che la societa’ ha lasciato invariato il suo obiettivo di raggiungere in questo esercizio una crescita inferiore al 5% (in modo organico). A livello consolidato il bilanciamento tra l’acquisizione di Vincor e il deconsolidamento della birra e

dell’ingrosso dovrebbe causare una riduzione del fatturato del 30% circa.

Q1-07 results of the world leader in wine production were not very positive, even if we are analysing the seasonally less significant quarter of the year. Constellation Brands just deconsolidated its wholesale business in the beer segment and therefore starting from this FY consolidated results will be much closer to wine division.

To be very clear we should also say that CBrands left unchanged its target to reach a 5% organic growth. At consolidated level, the contribution of Vincor and the deconsolidation of the beer business should generate a 30% reduction in sales.

Perche’ CBrands non e’ andata bene: (1) il mercato inglese; (2) un processo di de-stocking (svuotamento del canale distributivo) negli Stati Uniti.

Quali sono state le crescite del business vino nelle diverse zone del mondo?

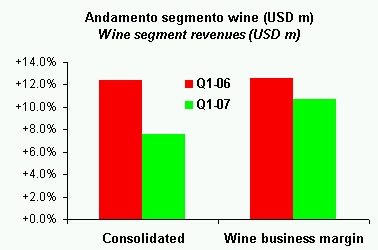

– il fatturato consolidato fa -22% per effetto dei deconsolidamenti. In termini organici (cioe’ su basi confrontabili) fa -2%.

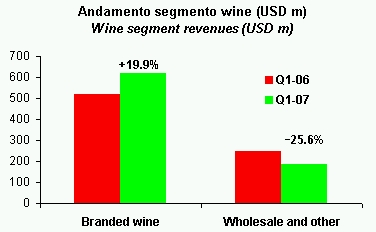

– il segmento “branded wine” fa +20%, pero’ sarebbe a -8% senza acquisizioni e senza l’effetto dei cambi;

– questo -8% si suddivide in: -13% in USA (destocking, anche se continuano a dire che il mercato e’ buono) e +11% in Europa (incluso UK).

What are the reasons of Cbrands poor performance? (1) the UK market; (2) a de-stocking process in the US.

Which are the different growth rate of the business around the world:

– consolidated sales were -22% due to consolidation perimeter. In organic terms, or on a comparable basis, the trend was -2%.

– the branded wine segment is +20%, but it would be -8% without acquisitions and the favourable foreign exchange effect.

– This -8% would be broken down in: -13% in USA (destocking, even if they continue to say that the market conditision remain good) and +11% in Europe (including UK).

Finiamo con quello che Constellation Brands si aspetta per il 2007: incremento del fatturato in termini organici positivo ma meno del 5%, il che implica che i prossimi trimestri dovrebbero essere migliori (quindi con riferimento all’Inghilterra e agli USA). Nonostante questo si attendono una riduzione degli utili nell’intorno del 20% da USD1.68 per azione a circa USD1.30-1.40.

Finally, the outlook. Constellation brands still expects a 2007 with a low-single digit increase of sales in organic terms, which implies an improvement of the trading conditions for the rest of the year. However, the profits should be lower by around 20% from USD1.68 of last year to the USD1.30-1.40 range for this one.