File Google spreadsheets.

Prima di passare ai numeri mi corre l’obbligo di ringraziare GIV e la sua responsabile per la comunicazione Tiziana Mori per avermi inviato il bilancio. Il 2007 e’ stato un buon anno per GIV, che ha confermato la sua leadership tra le aziende Italiane del settore con una progressione del fatturato superiore al 10%, con un buon andamento sia in Italia che all’estero, che come sapete per GIV e’ un’area chiave. In questo processo, il gruppo ha dovuto subire un aumento del capitale circolante, che ha portato l’indebitamento a 117m (da 104m), mentre e’ stato portato a termine l’operazione Bolla. In base a questa operazione, mentre GIV continua a fornire il prodotto Bolla a Brown-Forman per il mercato americano (EUR20m), ha cominciato a distribuire il prodotto in Italia. Inoltre, l’Istituto di Sviluppo Agroalimentare, società appartenente al Ministero dell’Agricoltura, e’ intervenuta con un apporto di EUR10m, condividendo con GIV quasi la meta’ dell’investimento in Bolla. Altri eventi importanti stanno però capitando: i due soci principali di GIV (CIV e Cantine Riunite) si sono fusi tra loro con effetto dal 1/8/2008. Questo ha portato il Gruppo a modificare il progetto di evoluzione societaria a suo tempo approvato. Infatti, in GIV Spa (che gestisce dal 1/1/2006 il ramo d’azienda commerciale) verranno conferite anche i rami d’azienda agricolo e produttivo (vigneti e cantine) a completamente del progetto a suo tempo previsto. La presenza, di un socio di riferimento (Cooperativa unificata fra Riunite e Civ) e che si appresta a divenire socio unico del Gruppo, modifica completamente lo scenario. Infatti, GIV Spa, che comunque manterrà una propria autonomia societaria e gestionale resterà legata alla nuova proprietà cooperativa del Gruppo. Per quanto riguarda il 2008, GIV prospetta una annata difficile, causa il difficile scenario economico e i problemi derivanti dalla svalutazione del dollaro… ma passiamo ai numeri.

Before moving to the numbers I would like to thank GIV and its media representative Tiziana Mori for having sent through the company report. 2007 has been a good year for the GIV, which has confirmed its leadership among Italian wineries with a progression of sales exceeding 10%, with a good performance both in Italy and abroad, which as you know for GIV and very important. In this process, the group had to undergo an increase in working capital, which affected net debt (up to 117m from 104m), and while it completed the acquisition of Bolla. Based on this, while GIV continues to supply Bolla products to Brown-Forman for the American market (EUR20m), it began to distribute the product in Italy. In addition, a stake in the company was bought by a state-owned firm for EUR10m, sharing with GIV nearly half of the investment in Bolla. Other important events are however happening: the two main shareholder of GIV (CIV and Canine Riunite) have decided to merge and this will lead GIV SpA to add to the commercial function also the production activity, and to remain in the hands of a new and larger cooperative. Regarding 2008, GIV announced a difficult year, due to the difficult economic scenario and problems arising from the devaluation of the dollar… but let’s move to the numbers.

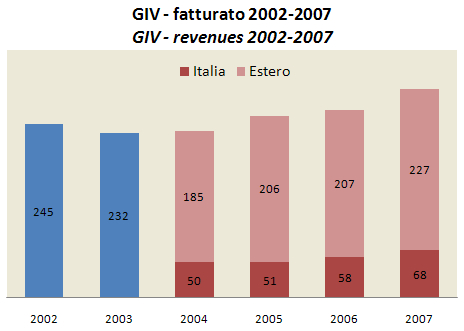

Il fatturato e’ cresciuto dell’11.4% a EUR294, di cui EUR68m in Italia (+17%) e EUR227m all’estero (+10%). La relazione non fornisce un dettaglio dell’apporto di Bolla, ma e’ presumibile che il forte rialzo in Italia sia da attribuire almeno in parte all’inizio della distribuzione del prodotto a marchio Bolla in Italia. Resta il fatto che il fatturato di GIV ha cominciato a crescere in modo significativo e, direi, piu’ velocemente di tutti le altre aziende leader.

Sales grew by 11.4% to EUR294m, of which EUR68m in Italy (+17%) and EUR227m abroad (+10%). The report does not provide a detail of the contribution of Bolla, but we argue that the sharp rise in Italy is to be attributed at least partly at the distribution of Bolla. However, the turnover of GIV has grew significantly and, we must say, it grew faster than all the other leading wine companies in Italy.

I margini sono rimasti stabili intorno al 7% a livello di MOL su fatturato. Va ricordato che GIV resta una cooperativa e che quindi ha dei margini che tengono conto dell’effetto ristorno che consiste nel riconoscere ai soci una liquidazione piu’ elevata dei vini e delle uve apportate (circa il 52% del totale). Il MOL ha comunque raggiunto EUR21m, +7% rispetto al 2006, l’utile operativo e’ sceso del 2% EUR11m (a causa dell’incremento degli ammortamenti. L’utile netto di EUR2.3m si riduce rispetto ai EUR2.9m del 2006 a causa dei maggiori oneri finanziari e degli interessi di minoranza (cioe’ la parte di utili che spetta a chi detiene % di minoranza in alcune aziende del gruppo, vedi operazione Bolla).

Margins remained stable at around 7% for EBITDA on sales. It should be noted that GIV remains a cooperative and therefore its margins are affected by the procedure to pay shareholders through a liquidation of higher purchasing price for wines and grapes delivered (about 52% of total). The EBITDA reached EUR21m, +7% compared to 2006, operating profit dropped by 2% EUR11m (due to depreciation). The net profit of EUR2.3m compared to EUR2.9m 2006 because of higher financial charges and minority interests (ie the portion of earnings that minority shareholding in certain companies in the group are entitled to receive).

Il capitale investito sale a EUR203m da EUR179m del 2006 a fronte di un aumento del capitale circolante da EUR82m a EUR98m, a causa di un aumento sia dei crediti vs. clienti (tempi di pagamento da 84 a 95 giorni) che del magazzino (da 92m a 104m, un aumento esattamente allineato a quello del fatturato), solo parzialmente compensato dai maggiori debiti verso fornitori. Questo aumento di EUR24m del capitale investito e’ stato finanziato per EUR10m dall’investimento esterno in Bolla, per EUR1m con un maggiore patrimonio netto (utili non distribuiti) e per EUR13m dall’incremento del debito da EUR104m a EUR117m (un livello per nulla preoccupante, peraltro).

The capital invested rose to EUR203m from EUR179m in 2006 against an increase in working capital from EUR82m to EUR98m, due to an increase in both loans vs. customers (receivable days from 84 to 95 days) and of inventories (from 92m to 104m, an increase exactly aligned to that of turnover), only partially offset by higher debts to suppliers. This increase in capital invested EUR24m was funded for EUR10m with the investment in Bolla by an external shareholder, EUR1m with equity (retained earnings) and EUR13m with the increase of debt from EUR104m to EUR117m (a level not at all worrying , by the way).

Infine, vi mostro il grafico di confronto tra GIV e il campione Mediobanca, dove potete vedere che GIV sta gradualmente riguadagnando il terreno perduto. Dati i grandi marchi che possiede e data la sua connotazione nazionale, potrebbe essere un’azienda molto più profittevole. Per far si che ciò avvenga è necessario un miglioramento sia sul lato commerciale che sul fronte del contenimento dei costi. Speriamo che la fusione tra Riunite e CIV ed il nuovo disegno organizzativo, considerate le maggiori dimensioni e la possibilità di generare sinergie possa dare un ulteriore impulso al gruppo.

Finally, I show you the comparison chart between the GIV and the sample of Mediobanca, where you can see that that GIV is gradually regaining the ground lost. GIV holds strong brands and a national presence which could be the source of higher profits. To achieve it, the group should be more effective in its commercial policies and generate more cost synergies, also on the back of the newe organisation.