E alla fine Foster’s decise di non vendere piu’ la divisione vino, ma di mettere in piedi un processo di ristrutturazione. E’ questa la conclusione della “wine review”, cioe’ dell’esame che il nuovo management di Foster’s ha condotto dopo le rilevanti perdite registrate a giugno, quando fu costretta a svalutare il valore dell’avviamento delle passate acquisizioni. Come mai l’azienda e’ tornata sui suoi passi? Semplice: non ci sono compratori al prezzo desiderato. Poi, come vedremo dal post, la divisione vino di Foster’s e’ stata molto aiutata dai cambi nel corso del primo semestre fiscale (Giugno-Dicembre 2008). A cambi pari avrebbe registrato un calo del fatturato del 3% e un calo dell’utile operativo dell’11%, dovuto soprattutto al calo dei volumi del 6%. Invece, la svalutazione del dollaro australiano ha aiutato i conti: alla fine del semestre la divisione vino segnava un +3% di fatturato a 1.16 miliardi di dollari australiani e un +10% dell’utile operativo a 243 milioni di dollari.

Foster’s has finally decided not to sell its wine business, but to start a restructuring process . This is the conclusion of the “wine review” started after the significant losses in June, when Foster’s was forced to devalue the goodwill of past acquisitions. Why the company is stepping back? Simple: there are no buyers. Then, as we will see, the wine division was helped by exchange rates in H1 (June-December 2008), which allowed good results. With the same rates than H1-07/08, turnover would have declined by 3% and operating profit by 11%, due primarily to lower volumes of 6%. Instead, the devaluation of the Australian dollar has helped the accounts: sales marked a +3% to 1.16 billion Australian dollars, while EBITS was +10% at 243 million dollars.

Cosa dicono del futuro? La sfida nel mondo del vino e’ riuscire a passare sul canale al dettaglio rispetto all’Horeca, in un contesto di “trading-down” dei consumatori. Per questo la ristrutturazione (che costera’ tra 330 e 415 milioni di dollari australiani, tutti nella seconda meta’ dell’anno) mira a separare la divisione vino da quella birra, a ridurre i costi di AU$100 milioni all’anno dal 2011 (meno circa 60 milioni di costi aggiuntivi che arrivano dalla parte birra) e a vendere alcune proprieta’ marginali (oltre ad alcuni vigneti).

What about the future? The challenge in wine sector is to move from on-trade to offtrade and to face the “trading down” of consumers. For this restructuring (which will cost between 330 and 415 million Australian dollars, all in the second half) Foster’s aims to separate the wine division from beer, to reduce costs by AU$100million per year by 2011 (but additional 60 million costs will come from the sepapration from beer distribution structure) and to sell some marginal properties (along with some vineyards).

Analizzando le vendite per area geografica, Foster’s fa notare quanto segue: (1) in Australia il gruppo e’ quasi tornato a crescere come il mercato e fa +6% a volume e valore nel segmento imbottigliato, mentre sta gradualmente uscendo dal segmento dello sfuso (-43% volumi a 0.4m di casse); (2) in Asia Foster’s ha subito un calo del 12% dei volumi a 0.8m di casse; (3) in USA Foster’s ha visto un calo del 7% delle spedizioni (-6% in Canada), principalmente a causa della debolezza di Beringer White Zinfandel. I problemi sembrano concentrarsi nella fascia sopra i 10 dollari, a detta dell’azienda. (4) in Europa, i volumi sono stati in crescita del 5% nel Regno Unito, mentre sono crollati nei paesi nordici (-28%) anche a causa dell’interruzione della distribuzione con V&S (che e’ stata comperata da Pernod Ricard).

Looking at sales by geographical area, Foster’s highlighted the following: (1) in Australia it is back in line with market trends, with +6% in volume and value in the segment bottled wine, while it is gradually coming out of the segment of bulk wines (-43% in volume of 0.4m cases), (2) Foster’s in Asia fell by 12% in volumes to 0.8m cases, (3) in the U.S. Foster’s has seen a decline in the 7% of deliveries (-6% in Canada), mainly due to the weakness of Beringer White Zinfandel. The problems seem to concentrate in the range above $10, according to the company. (4) in Europe, volumes were up 5% in the UK, but slumped in the Nordic countries (-28%) also due to the end of the distribution agreement with V & S (which was bought by Pernod Ricard) .

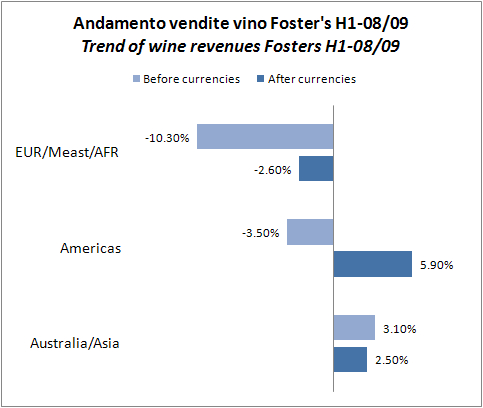

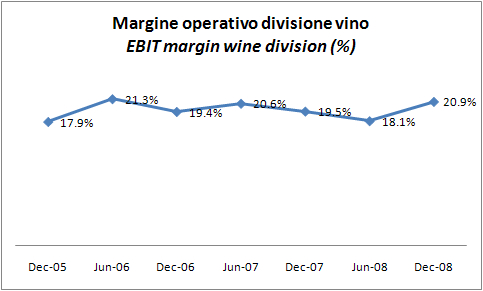

I numeri sono quelli che vedete nei grafici: i volumi sono giu’ del 6% a 19.9m di casse, soprattutto a causa del mercato europeo e americano. In tutti i mercati Foster’s e’ riuscita a migliorare il prezzo mix (tra i 3% e il 6%), mentre un forte impluso e’ stato dato dall’effetto cambio sia in Europa (+8%) che in USA (+9%). Il quadro generale e’ meno drammatico di quello che si potrebbe immaginare. Come vedete dal grafico dell’andamento delle vendite per area geografica e’ soltanto nettando per l’effetto cambi che si coglie veramente il cattivo andamento di Foster’s: -10% in Europa e -3.5% in USA. Lo stesso discorso vale per i margini, che sembrano in crescita dal 19.5% al 20.9% (primo semestre 2008-09 contro primo semestre 2007-08): in realta’ ai cambi di questo semestre il margine dello scorso anno sarebbe stato non 19.5% ma 22.9%… e quindi il margine sarebbe calato, e non di poco. The numbers are the ones you see in the graphs: volumes fell by 6% to 19.9m 9-liter cases, mainly because of European and American markets. In all markets Foster’s managed to improve the price mix (between 3% and 6%), while a strong help was given by the exchange rates in Europe (+8%) and USA (+ 9%). The general framework is less dramatic than one might imagine. As you can see from the graph of sales by geographic area it is just netting for the effect of exchanges rates that you can feel how bad was the performance: -10% in Europe and -3.5% in USA. The same is for EBIT margin, which seems to grow from 19.5% to 20.9% (first half of 2008-09 against the first half of 2007-08): in fact using the exchange rates of H1-08/09 for the previous one, the comparison would be with 22.9%, not 19.5% …and then the margin would have gone sharply down.

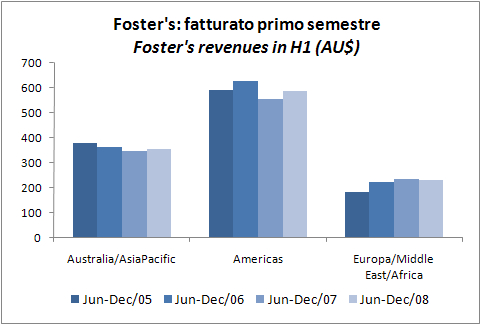

Passando brevemente ai grandi numeri, il consolidato Foster’s di Luglio-Dicembre 2008 mette in luce un aumento di fatturato del 2% (-1% a cambi costanti) a AU$2.4 miliardi, un utile operativo in crescita del 4% (-2% a cambi costanti) a AU$663 milioni e un utile netto di AU$411 milioni (+4%, -1% a cambi costanti). Il debito e’ salito da AU$2.4 miliardi a AU$3 miliardi a dicembre 2008.

Turning briefly to consolidated numbers, Foster’s H1 showed an increase in turnover of 2% (-1% at constant exchange rates) to AU$2.4 billion, operating profit grew by 4% (-2 % at constant exchange rates) to AU$663 million and net profit reached AU$ 411 million (+4%, -1% at constant exchange rates). Debt increased from AU$2.4 billion to AU$3 billion in December 2008.