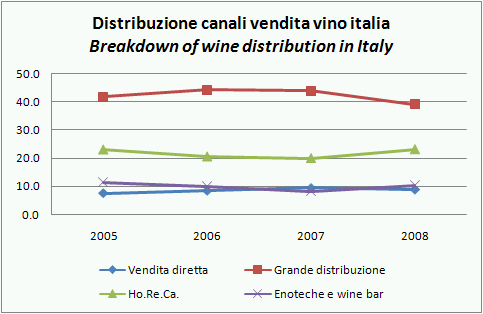

Lo studio Mediobanca include come sempre una parte sui canali distributivi, cosi’ come comunicati dalle aziende che partecipano al sondaggio. Quest’anno i risultati sono relativi all’81% del campione, a sua volta il 48% del mercato del vino italiano. Quindi stiamo parlando (come lo scorso anno) di una copertura di circa il 40% del mercato. Essendo questo il quarto anno che tracciamo, possiamo iniziare a fare qualche interessante confronto temporale, tenuto conto che la composizione cambia un pochino di anno in anno (il sondaggio Mediobanca ha aumentato il numero di aziende, allargando il limite a EUR20 milioni di fattuato annuo). Da questa analisi (tutti i numeri sono delle percentuali!) escono delle risultanze talvolta contrastanti con quelli che immaginiamo essere i trend. In particolare: (1) la GDO sembra perdere quote di mercato rispetto al passato; (2) il canale Ho.re.ca. e le enoteche starebbero guadagnando quote di mercato; (3) la distribuzione del vino italiano sembra andare sempre di più verso il canale indiretto (importatore e distributore indipendente rispetto a distribuzione propria). Quanto sono le quote di mercato per canale (trovate le torte alla fine)? Totale vino: 39% GDO, 23% Horeca; 10% enoteche/winebar. Grandi vini (oltre 25 euro): Horeca 46%, Enoteche/Winebar 28%, Vendita diretta 12%, GDO 9%.

Mediobanca review includes a survey on distribution channels. This year the results are relative to 81% of the sample, which is 48% of the market for Italian wine. So we are talking about (like last year) a coverage of about 40% of the market. As this is the fourth year that we trace, we can begin to make some interesting comparisons, provided that the composition changes slightly from year to year (the survey Mediobanca has increased the number of businesses, expanding the limit to EUR20 million annual turnover). From this analysis (all numbers are percentages!) we get some contradictory findings with those that we imagine to be the trend. In particular: (1) the large retailers seem to lose market share, (2) the restaurant/catering and wine stores would be gaining market share, (3) the distribution of Italian wine seems to go increasingly towards the indirect channel (importer and independent distributors). How are the market shares by channel (pies at the end)? Total wine: 39% GDO, restaurant/catering 23%, 10% wine shop. Superpremium wines (more than 25 euro): 46% restaurant/catering, Wineshop/Winebars 28% Direct sales 12%, large retailers 9%.

La distribuzione in Italia di questo 40% “top” del mercato puo’ ben essere interpretata come l’orientamento distributivo dei maggiori operatori del vino. Come vedete sembra che la grande distribuzione stia perdendo quote di mercato, particolarmente questo ultimo sondaggio, passando dal 44% al 39%. Tutto questo movimento è da attribuire alle aziende vinicole, in quanto per le cooperative continuano a pesare per il 50% circa (49.3% per la precisione). Questa perdita di quota è andata a beneficio del canale Ho.Re.Ca. che passa dal 20% al 23% e delle enoteche e wine bar che passano dall’8.3% al 10.4%.

The distribution in Italy of this 40% “top” of the market may well be interpreted as the orientation distribution of the major players in the wine business. As you can see it appears that the large retailers are losing market share, particularly this last survey, moving from 44% to 39%. The movement is driven by private wineries, as for the cooperative the weight remains about 50% (49.3% to be precise). This loss of share was at the benefit of restaurant/catering (from 20% to 23%) and wine shops/wine bars (from 8 .3% to 10.4%).

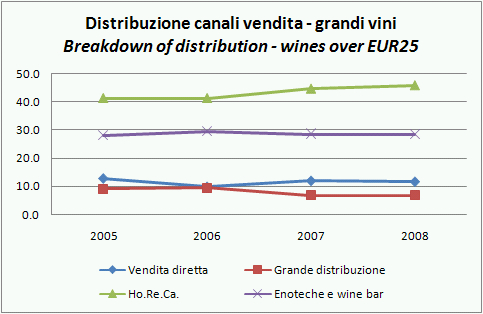

La situazione dei grandi vini è come ben sapete diametralmente opposta, anche se le tendenze non sono dissimili. La grande distribuzione resta relegata al 7% del mercato, cosi’ come le enoteche che sono stabili al 29%. Il canale Ho.Re.Ca. guadagna dal 44.6% al 45.8%. Anche in questo caso le cooperative non si comportano come le aziende vinicole: nel loro caso, le vendite in GDO stanno crescendo (ma partono da un livello molto basso, intorno al 4%) mentre perde peso il canale dell’enoteca wine/bar, che passa dal 32% al 29% del totale.

The situation of super premium wines is as you know diametrically different, even if the trends are not dissimilar. Large retailers are still relegated to 7% of the market and the wineries are stable at 29%. The channel restaurant/catering gains from 44.6% to 45.8%. In this case, the cooperative does not behave like the private wineries: in their case, sales are growing in large retail surfaces (but start at a very low level, around 4%), while while the channel wineshop/winebar lost weight, passing from 32% to 29% of the total.

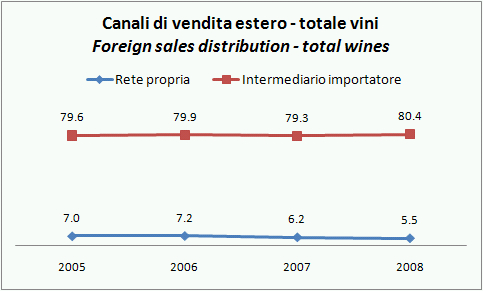

Passiamo alla distribuzione estera. Qui le conclusioni sono le stesse dell’anno scorso. Le aziende italiane stanno abbandonando le proprie strutture distributive per affidarsi a terzi. L’80% delle vendite estere è fatto con un intermediario importatore per il totale del mercato, quota che cresce all’88% per i grandi vini. La distribuzione diretta vale soltanto il 5.5% delle esportazioni. È un fattore negativo o positivo? La distribuzione diretta significa costi di struttura e poca flessibilita’, ma in cambio restituisce grande stabilita’ e visibilita’. Utilizzare un intermediario consente di mantenersi flessibili in cambio di un margine inferiore e con il rischio di rimanere a terra se il rapporto viene interrotto (di recente il distributore dei vini Antinori in USA UST è stato acquisito dalla Altria-Philip Morris).

Foreign distribution. Here the conclusions are the same as last year. Italian companies are abandoning their direct distribution structures to rely on third parties. 80% of sales are carried out through independent distributors (88% for superpremium wines). Direct distribution is only 5.5% of the exports. It is a positive or negative factor? Direct distribution means structural costs and little flexibility, but in return gives great visibility and control. Using a distributor you are much more flexible but you lose margin and you are at risk if the agreement is terminated (recently the US distributor of Antinori wines UST was acquired by Altria-Philip Morris).